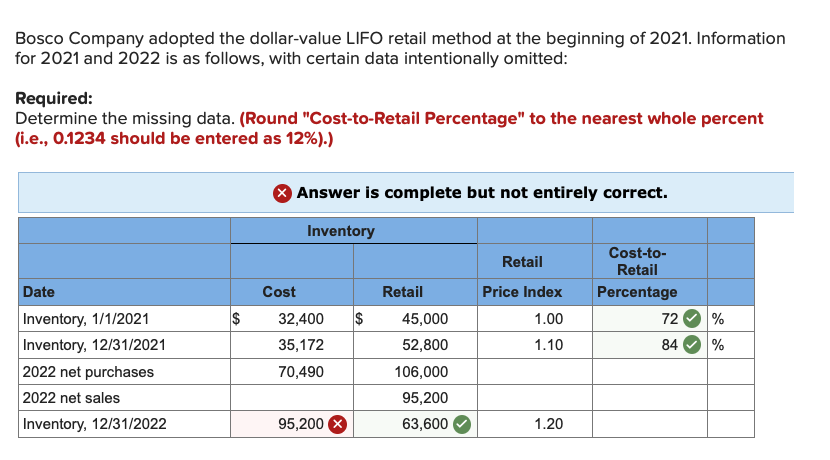

In an inflationary environment, it can more closely track the dollar value effect of cost of goods sold (COGS) and the resulting effect on net income than counting the inventory items in terms of units. Like specific goods pooled LIFO approach, Dollar-value LIFO method is also used to alleviate the problems of LIFO liquidation. Under this method, goods are combined into pools and all increases and decreases in a pool are measured in terms of total dollar value.

Learn with 30 Dollar Value LIFO flashcards in the free Vaia app

For instance, if in year 1, you have 10 units of product A and in year 2, you add 5 more units, then those 5 units form a layer over the base stock of 10 units. The Dollar Value LIFO (Last-In, First-Out) is a business accounting technique used to manage inventory and calculate the cost of goods sold. It may seem complex at first, but as you delve deeper, you’ll appreciate its utility and elegance. An eligible small business may elect to use the simplified dollar-value method of pricing inventories for purposes of the LIFO method. Vaia is a globally recognized educational technology company, offering a holistic learning platform designed for students of all ages and educational levels.

Interpretation of Dollar Value LIFO Formula

One thing worth mentioning again is that dollar-value LIFO pools the inventory up. In simple words we will have one total figure of all the different types of inventory we like to have in one pool. Dollar-value LIFO is a modification of traditional LIFO method in which ending inventory is measured on the basis of monetary value of units instead of quantity of units held. The base year is 2021, and you have 100 units in inventory that you purchased for $10 each, so your total base-year inventory cost is $1,000.

Impact on Financial Statements

- When combined with the $15,000 cost of the base layer, Entwhistle now has an ending inventory valuation of $34,800.

- The ‘layer’ concept and ‘base-year’ concept are inherent parts of Dollar Value LIFO.

- Dollar-value LIFO places all goods into pools, estimated in terms of total dollar value, and all reductions or increments to those pools are estimated in terms of the total dollar value of the pool.

- By the end of the year company had 1000 units of Item 1 and 5000 units of Item 2.

- One thing worth mentioning again is that dollar-value LIFO pools the inventory up.

The diversity in products in inventory pools allows this industry to smoothly transition from one year’s collection to another, without dealing with eroding layers. It helps the companies to account for the impact of inflation on their financial reporting. The adoption of Dollar-Value LIFO can lead to significant changes in a company’s financial statements, particularly in the balance sheet and income statement. By valuing inventory at the most recent costs, this method often results in lower ending inventory values compared to other inventory valuation methods like FIFO (First-In, First-Out).

User account menu

This method may only suit specific industries where inventory quantity and value changes aren’t closely correlated. Additionally, companies should avoid creating unnecessary inventory pools to prevent increased complexity and costs. By using the latest prices first, cost of goods sold — or COGS — under LIFO is higher, and taxable income is lower, when compared to FIFO.

LIFO Liquidation

Dollar-value LIFO is an accounting method utilized for inventory that follows the last-in-first-out model. Dollar-value LIFO involves this approach with all figures in dollar amounts, as opposed to in inventory units. It gives an alternate perspective on the balance sheet than other accounting methods, for example, first-in-first-out (FIFO). Remember, this is a simplified example and doesn’t take into account some of the complexities that can arise when you have multiple inventory pools or when prices decrease. Always consult with an accounting professional or financial advisor when dealing with inventory valuation. The LIFO retail inventory method employs the Last-in, First-out costing method to estimate ending inventory costs.

This tax deferral can be particularly advantageous in times of inflation, as it allows businesses to retain more cash for operations and investments. Under standard LIFO, you must track your inventory by units, even if you combine similar units into pools. This requires you to track the cost of all purchases and keep records on how you use up your inventory pools through sales. If you adopt the DVL method, you make a physical count of ending inventory and apply the proper DVL cost. The DVL method allows you to determine the proper cost without referring to any flow assumptions for inventory units. In other words, you don’t have to worry about applying costs in LIFO sequence to the units you sell during the year.

It allows companies to match current costs with current revenues, providing a more accurate reflection of profitability. The pools created under this method are, therefore, known as dollar-value LIFO pools. Under the regular LIFO method, inventory is measured in units and is priced at unit prices. Under the dollar value LIFO method, inventory is measured in dollars and is adjusted for changing price levels.

Only if such information is impossible to locate can the current cost also be considered the base year cost. Specific Identification is a method that assigns actual costs to individual inventory items. This approach is highly accurate and is often used for high-value or unique items, such as luxury goods or custom machinery.

This added layer of transparency aims to give investors and stakeholders a clearer understanding of a company’s financial health and decision-making processes. Dollar-Value LIFO operates on the principle of valuing inventory in terms of dollars rather than physical units. This method aggregates inventory into pools based on their dollar value, which helps in simplifying the tracking of inventory layers.

To solve delayering problem, we use traditional LIFO’s modified approach called how to calculate outstanding shares. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network.